When it comes to navigating the intricate world of mortgages and loans, Dave Porter stands out as the go-to expert with over 40 years of unwavering dedication. He not only answers the call promptly but also goes above and beyond, tirelessly searching for multiple viable solutions to guide you towards a prosperous future and help you achieve your goals.

In today’s exclusive interview, we delve into Dave’s wealth of experience and expertise as a mortgage lender in the ever-evolving landscape of today.

Dave’s Experience: Dave, with over 40 years in mortgage lending, what significant changes have you witnessed in the industry over the years?

Shields, thank you for those kind words. I would like to acknowledge you and the LocalsGuide. You provide options, both print and online, for readers to learn more about local businesses and the opportunity for businesses to provide articles to inform the community. Thank you.

I’ve seen a variety of loan program changes over the years. Some have been good for the consumers, and some have not. I like financing alternatives to help buyers, but I don’t want it at the cost of them losing their credit or their house. There was a time when we had loans where we didn’t verify income or assets to buy a home, and it set up the system to fail. I hope we have all learned our lesson.

Perspective on Rates: You mentioned starting in lending when rates were 17.5%. How has this historical perspective shaped your approach to mortgage lending today?

Over the last 40 years, the average interest rate has been 7.74. Today we’re in the high sixes and low sevens. I feel that many got “rate shock” when they went up as quickly as they did. We have to remember, those low rates in the 3%, 4%, and even 5% range were artificial as the Fed lowered rates with the hope of stimulating the economy during Covid. Don’t forget that as rates decline, you always have the opportunity to refinance.

Home Price Dynamics: How do you see the interplay between artificially low rates during COVID, the Almeda Fire, and the resultant surge in home prices?

I’m going to stay in my lane. I’m a lender, not an economist nor a fortune teller but with that said, when rates are low, more can afford to buy, and with more demand, prices go up. One source says values have gone down 1.8%. When rates normalize, values settle. My opinion is we won’t see a drastic decrease in home values.

Toolbox Analogy: You compared a lender’s tools to a toolbox. Could you elaborate on the various tools lenders need and how they impact the lending process?

Not all lenders are the same. Some may have just a hammer or wrench. More tools can provide more options. Some lenders are only bankers using their own sources of funds, others are only brokers who go out and source funding. I’m pleased that loanDepot is a mortgage banker and broker. We have many lending solutions.

Investment Strategy: You mentioned some buyers are keeping low-rate loans and renting out their homes. Can you elaborate on this strategy and its implications?

Often buyers will sell their home and buy a nicer one. Many who have low rates may have an option; the lower payment could allow them to rent that home out and begin to build a passive income source.

Changing Down Payment Requirements on multi-unit properties: You mentioned changes in down payment requirements.

Recently conventional loans on multi-plexes (duplex, triplex, and fourplex) can now be purchased with 5% down instead of 15% down. I encourage folks to not forget about a multiplex purchase when thinking of buying a place to live.

AccessZERO Program: Can you delve deeper into loanDepot’s AccessZERO program, particularly how it assists those with high incomes and no down payment?

This program offers a regular FHA loan but then has a second mortgage that covers the down payment. In some cases, it can even cover the down and some of the closing costs. It can be for first-time home buyers but not required and unlike many other zero-down payment programs this does not have an income limitation. And the FHA has recently increased its maximum loan to $498,257.

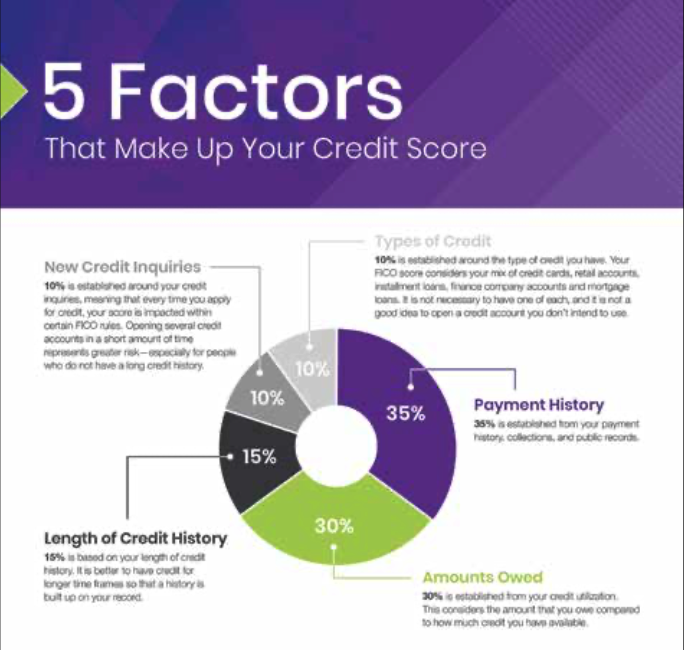

Credit Score Considerations: What’s a good credit score and how low can a score be and still get a home loan?

Scores above 800 are stellar. We can still do loans with much lower scores but it depends on the type of loan. For example, on a conventional loan or USDA we can go as low as 620. On an FHA loan, we can go to 580 and on a VA we can go as low as 520.

ADU and Additional Income: For those eyeing properties with ADUs for extra income, what options are available? And how does it affect qualification?

Lenders now can count part of the income of an accessory dwelling unit. The opportunity to help offset the mortgage is a game changer.

Oregon Bond Program: You mentioned the Oregon Bond program for first-time homebuyers. Despite higher rates, can you discuss its benefits and how it supports home purchases?

Not all lenders can offer this program. The rate advantage program is very attractive and currently in the low 6% range.

Co-buying Strategy: Co-buying is an interesting strategy. How should individuals approach this method and what considerations should they keep in mind?

Co–buying is a solid strategy. Where two or more like-minded folks “go in” on buying a home together. This should not be flippant but can serve as a way to join forces to own a home. I know of one company that does this “matchmaking” using a formal process.

Reasons for Refinancing: Dave, are people still refinancing and what are the common reasons for doing so in today’s market?

Yes, the reasons vary – from needing to take someone off the current loan (like in a divorce situation) or a cash-out to do a major remodeling project or to pay off/down high-interest rate installment and credit card debt or remove mortgage insurance.

Dave, thanks for sharing all this great information. Do you have any last thoughts or comments for our readers?

This can be a stressful process of buying a home and obtaining a mortgage. Be sure you have on your team people who are available and people you feel you can trust. Keep it local. Sellers and listing agents prefer a local lender and not a .com and you want more accountability from your lender partner. You have every right to “interview” a Realtor or lender. I am not stuffy with my clients, I let them know I’m lighthearted, look at my silly advertisement at the Medford Airport.

Equal Opportunity Lender. This information is not intended to be an indication of loan qualification, loan approval or commitment to lend. Loans are subject to credit and property approval. Other limitations apply. Rates, terms and availability of programs are subject to change without notice. State disclaimer: loanDepot.com, LLC NMLS ID 174457. www.nmlsconsumeraccess.org Licensed by the OR Division of Finance and Corporate Securities, Mortgage Lending ML-4972.| WA: Licensed by the WA State Department of Financial Institutions, Consumer Loan Company CL-174457.

———————

Dave’s success and availability to his clients weekends and evenings are due to his loving and supportive wife & family. Ten minutes after this photo was taken Dave was prequalifying someone for a loan!

Learn More:

loanDepot

Dave Porter NMLS 483876

—

541-708-4020